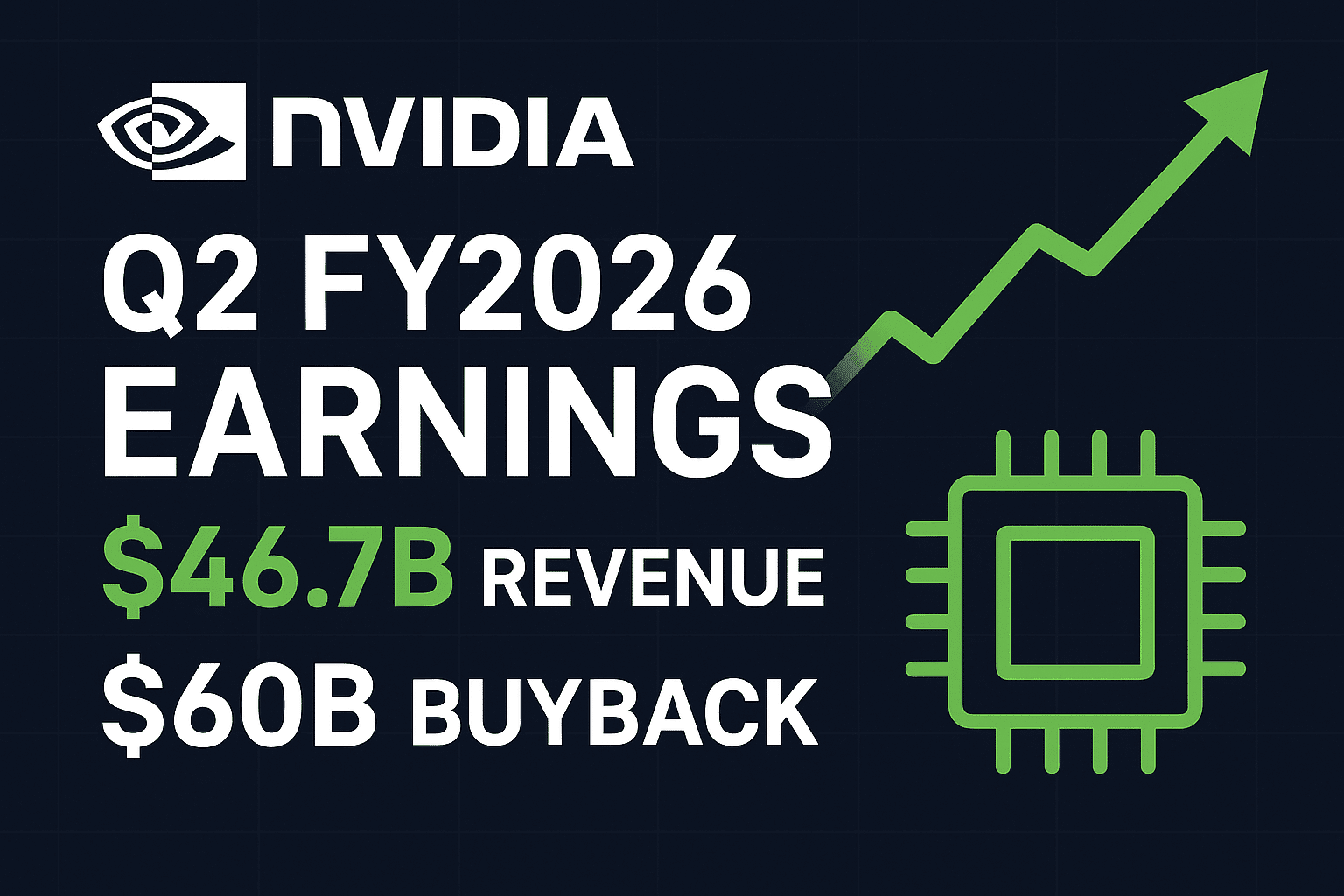

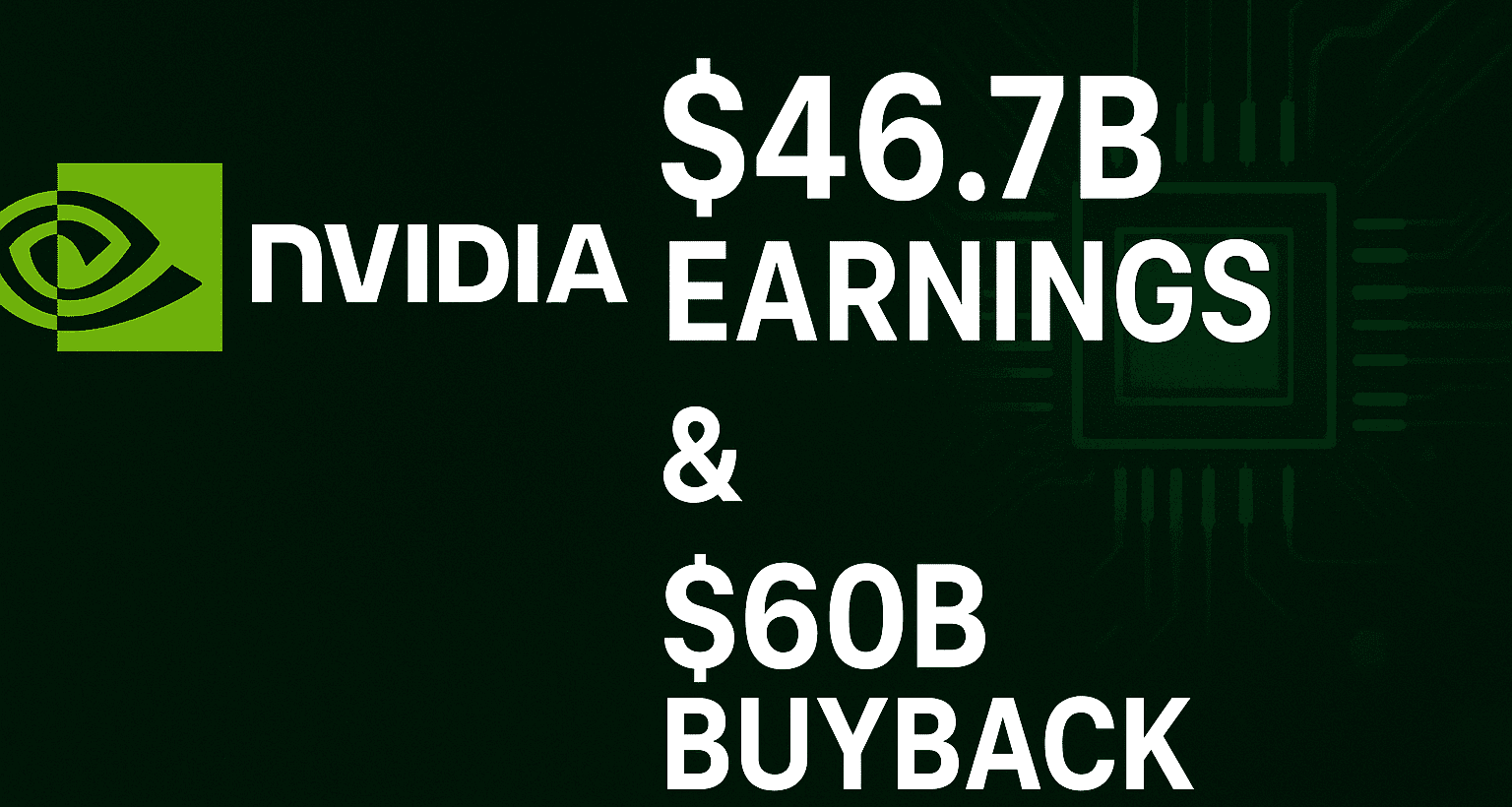

NVIDIA Q2 FY2025-26 Earnings

Featured: NVIDIA Q2 FY2026—$46.7B revenue and $60B buyback

Featured: NVIDIA Q2 FY2026—$46.7B revenue and $60B buybackNVIDIA (NASDAQ: NVDA) has once again captured headlines with a blockbuster Q2 FY2026 earnings report. The company reported $46.7 billion in revenue—up 56% year-over-year—and announced a massive $60 billion share buyback program. Despite the strong numbers, NVDA shares slipped in after-hours trading amid investor worries over slower sequential data center growth and lingering regulatory uncertainty around China chip sales.

Key Q2 FY2026 Highlights

- Total Revenue: $46.74B (+56% YoY, +6% QoQ)

- Data Center Revenue: $41.1B (+56% YoY)

- Net Income: $26.42B (+59% YoY)

- EPS: $1.05 (Non-GAAP), $1.08 (GAAP)

- Gross Margin: 72.4% GAAP, 72.7% Non-GAAP

- Blackwell Growth: +17% sequential

- Gaming: $4.3B (+49% YoY)

- Professional Visualization: $601M (+32% YoY)

- Automotive/Robotics: $586M (+69% YoY)

Data Center: The Engine of Growth

NVIDIA’s data center business remains its dominant revenue driver, contributing ~88% of total quarterly revenue. Adoption of the Blackwell GPU architecture drove sequential growth of 17%, which the company described as “extraordinary.” Still, data center revenue came in just under some analysts’ expectations (~$41.3B), signaling a modest cooling in sequential momentum compared with earlier explosive quarters.

Why sequential growth slowed

Analysts point to a mix of supply constraints, the transition cycle from older GPU architectures, and the impact of regulatory limits affecting sales to China. While demand remains strong, market expectations were extremely high—leaving little room for even small misses.

Gaming, Professional & Automotive

While data centers lead the way, NVIDIA’s other segments are performing well: gaming revenue rebounded strongly as RTX 40-series adoption increased, professional visualization rose year-over-year, and automotive/robotics continues to grow as OEMs and mobility providers integrate NVIDIA’s DRIVE and robotics platforms.

$60B Share Buyback: Management Shows Confidence

NVIDIA announced a $60 billion additional repurchase authorization—one of the largest buybacks on record. The move follows $24.3B returned to shareholders during the first half of FY2026 and signals management’s belief in the company’s long-term prospects. Coupled with a small dividend (recently maintained at $0.01 per share), the buyback should help support the stock through short-term volatility.

China H20 Chip Freeze & Geopolitical Risks

A major overhang this quarter was the lack of sales of the H20 AI chip to China:NVIDIA reported zero H20 sales to China this quarter due to U.S. export restrictions. The company released approximately $180M in reserved inventory to non-China customers. Reports indicate NVIDIA may negotiate a revenue-sharing arrangement (reported to be ~15%) to gain regulatory clearance—an outcome that could unlock an estimated $2–$5B in potential sales if approved.

Production of H20 was reportedly halted pending further approvals, and next-generation chips such as the Blackwell-based B30A are also subject to export consideration.

Why NVDA Stock Fell Despite Strong Results

NVDA shares fell between 2.5% and 4% after-hours on the report. The reasons were:

- Slight miss on data center expectations—the segment narrowly missed some street forecasts.

- Priced-for-perfection valuation—investors had extremely high growth expectations already priced in.

- Geopolitical uncertainty—China export restrictions create real revenue risk.

Q3 FY2026 Guidance & Outlook

NVIDIA guided Q3 revenue of approximately $54 billion ±2%, above analyst averages. Gross margins are expected to remain robust (mid-70s percentage range on a non-GAAP basis). This outlook reflects continued AI-driven demand for training and inference hardware even as certain markets remain constrained.

NVIDIA vs. Competitors

NVIDIA still dominates AI GPU training with an estimated 80–90% market share. Its CUDA developer ecosystem and partnerships with cloud hyperscalers create a competitive moat. Competitors such as AMD (MI300), Intel (various accelerators), and in-house chips from hyperscalers are making progress, but NVIDIA’s combination of software, hardware, and ecosystem remains the industry standard for now.

Key Metrics at a Glance

| Metric | Q2 FY2025-26 | Change |

|---|---|---|

| Total Revenue | $46.74B | +56% YoY / +6% QoQ |

| Data Center | $41.1B | +56% YoY |

| Net Income | $26.42B | +59% YoY |

| EPS (Non-GAAP) | $1.05 | (~$1.04 excl. H₂O) |

| Gross Margin | 72.7% | — |

| Blackwell Growth | +17% QoQ | — |

Risks & Investor Takeaway

Key risks include ongoing China export restrictions, potential slowing sequential growth in the data center market, and rising competition. Nevertheless, NVIDIA’s leadership in AI GPUs, profitable segments, and the massive buyback make it a prominent long-term play in the AI era. Investors should weigh near-term volatility against long-term structural growth driven by AI infrastructure.

Related Reading

Conclusion

NVIDIA’s Q2 FY2026 results reaffirm its central role in powering the AI revolution: record revenue, sizable profits, and aggressive shareholder returns. Yet short-term headwinds—particularly regulatory restrictions on China sales and the possibility of more moderate sequential data center growth—introduced volatility. For long-term investors focused on AI infrastructure, NVIDIA remains a core holding, with the recent $60B buyback signaling management’s confidence in the company’s growth runway.

for more financial information click here